In Brief

- The Big Issue: Australian banks are running on 30-to-40-year-old systems that make launching new products incredibly slow and expensive.

- The Catalyst: Strict rules from APRA (especially CPS 230) and Open Banking regulations are forcing banks to upgrade now.

- The Strategy: Instead of risky “Big Bang” system replacements, banks are moving slowly by copying data to parallel systems or shifting minor tasks first.

- The Technology: Moving away from bulky mainframes into the cloud, using APIs, and building real-time data streams that can support modern AI tools.

- The Payoff: Massive drops in maintenance costs, faster product rollouts (days instead of months), and safer, real-time banking for customers.

Imagine that a bank’s core is akin to its beating heart, managing everything from account openings and balance checks to daily transaction processing. For many large and mid-size Australian banks, this heart was developed 30 to 40 years ago for a bygone era of overnight batch processing, leaving it under massive strain in today’s 24/7 digital world of instant taps, swipes, and digital wallets. Because every mobile app and fraud tool relies entirely on this central engine, upgrading it is the tech equivalent of open-heart surgery on a patient running a marathon, where a single misstep can freeze cards and shut down ATMs.

To avoid a catastrophic system failure, smart institutions are moving away from risky, all-at-once transplants and are instead “hollowing out the core,” using flexible cloud networks to take over the workload step-by-step to meet strict APRA CPS 230 rules and safely secure a real-time future.

While the current situation does not involve banks’ systems going haywire and stopping their operations, there’s another problem involved here. Namely, that these old systems simply aren’t fit for use in a modern environment, characterized as it is by demand for quick payments and customization options provided by apps. The issue at hand isn’t whether banks have to update their systems, but rather, how.

The Actual Failures of Traditional Core Banking

Legacy banking systems are not failing because they suddenly stop working. In fact, many of them continue to process millions of transactions every day. The real problem is that they were built for a different era and struggle to meet the speed, flexibility, and compliance demands of modern banking.

The Challenge of 40-Year-Old Technology

Many banks still rely on core systems built decades ago using programming languages such as COBOL. These systems were designed when banking transactions were processed in batches, often overnight after branches closed.

Today’s banking environment is very different. Customers expect instant payments, real-time account updates, digital wallet integration, and 24/7 banking access. Modern payment networks operate continuously, leaving little room for the overnight processing windows that older systems depend on. As a result, banks often find it difficult to deliver the speed and responsiveness customers now expect.

The “Spaghetti Integration” Problem

Over the years, banks have repeatedly modified their systems to accommodate new regulations, launch new products, and integrate acquired businesses. Instead of rebuilding the foundation, many institutions simply added new layers of technology on top of existing ones.

The result is a highly complex network of interconnected systems, often referred to as spaghetti architecture. In such environments, even a relatively small change, such as introducing a new loan product or adjusting interest rate calculations, can affect multiple systems. This requires extensive testing and validation, causing projects that should take weeks to stretch into months.

Because of this complexity, many banks spend nearly 80% of their technology budgets maintaining existing systems, leaving only a small portion available for innovation and digital transformation.

The Hidden Cost of Dark Data

One of the biggest limitations of legacy banking platforms is that valuable customer and transaction data often remains locked inside isolated systems and mainframes.

This information exists, but it is difficult to access, search, analyze, or use in real time. As a result, banks are unable to fully leverage their own data for advanced capabilities such as AI-driven customer insights, personalized financial services, predictive analytics, or sophisticated fraud detection.

In effect, large volumes of potentially valuable information remain “dark data,” stored but underutilized.

Growing Regulatory and Compliance Pressure

Modern banking regulations increasingly require institutions to demonstrate stronger operational resilience, better risk management, greater transparency, and secure data sharing.

In Australia, regulations such as APRA’s CPS 230 and the Consumer Data Right (CDR) framework are pushing banks toward real-time data accessibility, stronger operational controls, and improved interoperability. Legacy systems, originally designed long before these requirements existed, often struggle to support these expectations without significant upgrades or costly workarounds.

As regulatory demands continue to evolve, the limitations of traditional core banking systems become even more apparent, making modernization a strategic necessity rather than a technology upgrade.

Mainframes vs. Cloud Computing

To understand how modern banking looks, one needs to understand how the traditional system was developed. Cores used in traditional banks are said to be “monolithic.”

This means everything: the user interface, the loan logic, the account ledger, and data storage are glued together into one massive block of code. Change one piece, and the whole thing risks breaking.

Modern core systems use a decoupled approach built on cloud-native microservices.

Instead of one giant program, the bank is broken down into small, independent apps. For example, the tool that handles your savings account runs completely separately from the tool that manages your credit card. They talk to each other using fast, standardized interfaces called APIs.

By moving these tools to app secure cloud platforms like AWS or Microsoft Azure, banks gain incredible flexibility. When transaction volumes spike during major shopping holidays or corporate paydays, the cloud automatically adds computing power to handle the rush. As soon as the rush ends, the system scales back down to save on operational costs.

This shift also introduces real-time data streaming using platforms like Apache Kafka. Instead of processing transactions in big batches overnight, every single swipe, tap, or transfer is updated instantly. This real-time visibility is vital for satisfying modern consumers who expect immediate push notifications and accurate balances.

The Challenges of Upgrading a Bank’s Core Systems in Australia

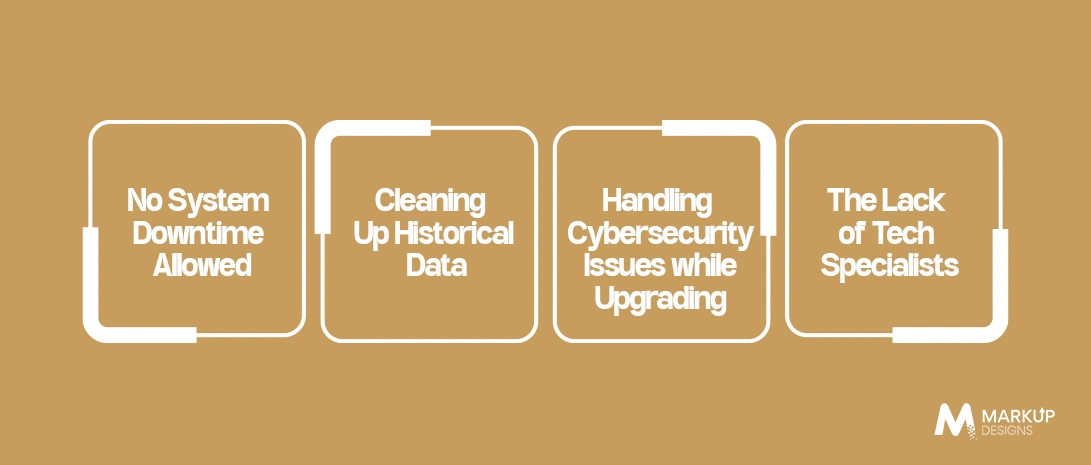

Reprogramming an entire bank’s core system is equal to changing out the engine of a commercial plane mid-flight. In the highly regulated environment of the Australian banking industry, engineers confront four monumental hurdles:

1. No System Downtime Allowed

Since the launch of the New Payments Platform (NPP), which operates continuously, the idea of a “maintenance window over the weekend” is obsolete. Any failure on the part of a bank’s system would cause immediate harm to its reputation and regulatory attention from the likes of ASIC.

Solution: Major banks are relying on a “Parallel Run.” Rather than powering down the mainframe over a Friday evening, the new cloud architecture is installed alongside the legacy platform. For three to six months, real-time operations are executed using both platforms. This allows engineers to find bugs, balance account ledgers to the last cent, and stabilize the system before the switchover.

2. Cleaning Up Historical Data

Over many years in business, banks create a lot of historical data, which is often messy and disorganized. Different account classifications use different tracking codes, and formatting rules have been changed many times over the years. Dumping all this messy data onto a freshly constructed cloud environment would immediately bring it crashing down.

Solution: Financial institutions make use of automated pipelines to sanitize all the information. Before anything is imported, the intelligent algorithms run through the documents, correct errors, and format all information according to the universally accepted ISO 20022 standard.

3. Handling Cybersecurity Issues while Upgrading

Upgrading a financial institution exposes it to all sorts of cybersecurity risks. As the specialists establish digital bridges to connect mainframe systems to the cloud, criminals are already actively searching for vulnerabilities in this transitional link.

Solution: Contemporary projects are designed using Zero Trust Architecture. It implies abandoning periphery security measures. Instead, the system automatically assumes that any and all attacks can come from anywhere. Thus, every request, whether inside or outside the company’s network, is verified and encrypted.

4. The Lack of Tech Specialists

Australia is suffering from a severe shortage of specialists capable of working with COBOL-based mainframe systems and modern cloud technologies. This is one of the reasons why projects tend to be delayed and exceed budgets.

Solution: The banking institution needs to adopt a hybrid team of internal and external experts who can implement the solution. The internal bank team can benefit from being mentored by cloud modernization experts since they have more experience in deploying such solutions. This ensures that any work done will be safe while educating the internal employees on maintaining the system for a very long time into the future.

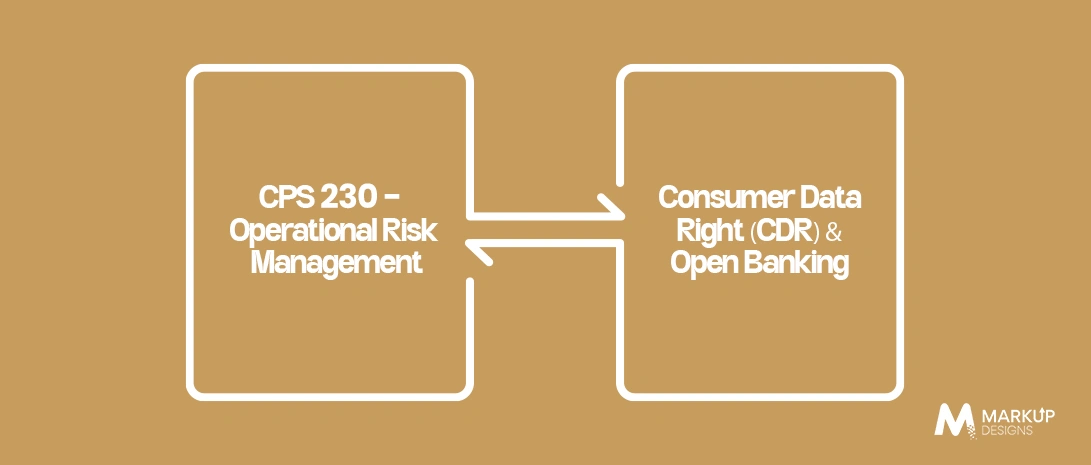

The Regulators Driving the Change: APRA CPS 230 & CDR

In Australia, upgrading your bank’s core infrastructure is not only a choice but a requirement mandated by two major laws.

CPS 230 – Operational Risk Management

Issued by the Australian Prudential Regulation Authority (APRA), the CPS 230 regulation has significant emphasis on operational risk management. The regulation requires that top-level executives of the bank map and regularly test their critical services in case of extreme scenarios.

This cannot be achieved using legacy cores due to the many steps involved. However, through a cloud-native approach, automation and tracing mechanisms will allow risk professionals to understand data flow and quickly transfer the processes to another cloud location should an emergency occur.

Consumer Data Right (CDR) & Open Banking

The Consumer Data Right gives the client ownership of their data.

By legislation, banks in Australia have the obligation to provide secure sharing of client information with trusted fintech applications upon request by the customer.

Traditional legacy mainframes were not designed to manage large volumes of data queries from outside. Adding external functions to the core results in system lag. The newest cores have API management capabilities, allowing for the instantaneous processing of thousands of data queries.

Real World Examples: How Australian Banks are Upgrading

Benefits become apparent by reviewing the practices of Australian banks implementing changes:

Image needed

1. Commonwealth Bank of Australia (CBA)

CBA has managed to successfully migrate its 61,000+ data feeds into a centralized cloud environment. This infrastructure manages over 157 data points daily in real-time mode. Thus, CBA is able to use the power of instant analysis to run sophisticated machine learning algorithms and predict fraud patterns within fractions of a second. Additionally, users get personalized financial advice through a mobile application.

2. National Australia Bank (NAB)

National Australia Bank used the method of “hollowing out” the core to achieve the desired results. It means that NAB did not migrate all processes but isolated secondary ones such as onboarding, rewards management, and loans origination and moved them to the cloud.

By limiting the scope of the ancient mainframe to only handling basic accounting ledgers, they cut down on operating costs, and improved speed to market by a wide margin.

3. Bank of Queensland (BOQ)

Modernization is key to survival for regional banks like BOQ. In the past, BOQ has operated using several different retail and commercial brands, each of which had its own independent legacy core. In a multi-year project, BOQ decided to consolidate its entire suite of sub-brands into one single, consolidated cloud ecosystem. With one platform, they were able to get rid of duplication and launch their digital products simultaneously across all of their sub-brands.

Strategic Advantage of Partnering with Markup Designs

Operating within the context of core modernization, one needs far more than a simple software purchase but rather requires engineering prowess and well-proven architecture parameters. Through engaging the services of Markup Designs, one can overcome this challenge, turning what was once a risk into a smoothly functioning business advantage.

Markup Designs provides a strategic advantage through the use of forensic legacy audit services that detail exact technical debts and any COBOL dependencies. This is achieved through migration frameworks that utilize parallel runs and Zero Trust security bridges to ensure absolutely no operational disruption whatsoever.

By integrating our unique engineering pods within your organization, Markup Designs takes care of your problem caused by the local technology shortage. The creation of API layers and microservices necessary for breaking away from structural rigidities is handled proactively by us without any disruption of your transactions.

Framework For Implementation: The Five Stages Of Success

At Markup Designs, we rely on a well-defined five-step implementation framework for guiding banks along the way:

Step 1- The System Audit

Use automated software to audit your legacy system infrastructure, map out your technical debt, and identify precisely where your oldest software is causing operational constraints.

Step 2- Strategy Selection

Determine whether you need to create an entirely new online brand (“Greenfield”) or adopt the “Hollow Out the Core” approach.

Step 3– Cloud Infrastructure Establishment

Set up your cloud architecture across multiple geographic jurisdictions in Australia.

Step 4- Compliance-by-design and Parallel Validation & Cutover

Embed all the necessary data tracking and security mechanisms directly into your architecture from the get-go. This will ensure that all your transactions are tracked automatically, simplifying APRA reporting.

Step 5- Parallel Validation & Cutover

Run your new cloud environment and old architecture in parallel until the new environment replicates the old architecture records flawlessly for weeks. After that, switch your production traffic seamlessly to the new environment.

The Cost of Upgrade vs. the Cost of Doing Nothing

While the upgrade process itself requires significant expenses, the cost of inaction is significantly higher.

Maintenance costs are high. Licensing fees, the high price of COBOL specialists’ work, and other expenses raise operating costs by 10% to 15%. What’s more, the inability to implement digital improvements quickly lets nimble neobanks poach your customers. Considering possible fines for missing resiliency deadlines, the core banking upgrade ceases to be merely an IT cost but becomes a strategic necessity.

Drive Your Digital Transformation Forward

Are evolving APRA regulations stretching your infrastructure to its limits? Partner with Markup Designs to simplify your legacy systems, eliminate operational risks, and build a scalable foundation ready for the future of finance.

Conclusion

Core banking upgrade in Australia has now become a must-have business change.

As we head into a highly integrated, digital-first banking landscape, the institutions that break free from legacy technical debt will lead the market. Building a cloud-native, real-time infrastructure unlocks the speed needed to deploy advanced AI tools, protect consumer data, and launch competitive products quickly.

At Markup Designs, we specialize in helping financial institutions navigate this transformation journey safely. From forensic legacy software audits to building zero-trust API layers and resilient cloud microservices, our experienced engineering teams deliver your modernization goals with precision and minimal risk.

FAQ’s

1. What is core banking modernization, and why is it important right now?

Core banking modernization means replacing or re-architecting a bank’s foundational backend systems, which handle ledgers, account balances, and transactions, with cloud-native, API-first technology. It is vital right now because older mainframes cannot handle the real-time processing demands of the New Payments Platform (NPP) or the data-sharing rules of Open Banking.

2. How does APRA’s CPS 230 rule affect old core systems?

APRA CPS 230 requires banks to thoroughly map and continuously test their critical operations against unexpected outages. Older mainframes, with their complicated batch processing loops and hidden dependencies, make this impossible to track. Upgrading your core system provides clear, automated logging and instant backup failovers to ensure full regulatory compliance.

3. What is the “Hollow out the Core” strategy?

This is an approach where you don’t replace the entire mainframe at once. Instead, you move peripheral services, like onboarding, digital apps, and rewards systems, to the cloud first. This leaves the old mainframe to handle nothing but basic ledgers, which significantly reduces risk during the upgrade project.

4. How do data privacy updates impact bank architectures?

Privacy updates grant consumers more control over their records, including the right to have their data deleted upon request. Old monolithic systems duplicate user data across highly isolated databases, making it incredibly hard to locate and remove completely. Modern systems simplify this by using unified data setups that allow compliance teams to manage data controls globally.

5. Does a modern core banking system lower operational costs?

Yes. Shifting to cloud-native systems removes expensive mainframe hardware licenses and cuts down the manual work required for upgrades. It also lets banks scale their computing power up or down based on real-time transaction traffic, making infrastructure spending highly efficient.

Author's Perspective

As a digital transformation architect at Markup Designs, I have spent years helping businesses upgrade complex legacy systems. The Australian banking sector is particularly unique because it features incredibly demanding digital consumers alongside some of the strictest regulatory frameworks in the world.

In this environment, waiting for a perfect, risk-free moment to upgrade your core architecture is a mistake. That perfect moment does not exist. Technical debt grows more expensive every single day, silently slowing down your product rollouts and increasing your operational risk profile. The institutions finding the most success are those moving forward with an agile approach. By breaking systems down into microservices, focusing on compliance from day one, and working with deep engineering partners, banks can safely modernize their tools and secure a strong edge in the modern digital economy.

Discuss Your Project NowGaurav Goyal

Global Sales- VP

Insights Are Valuable & Execution is Priceless

You’ve read about the digital future. Now, let’s build the infrastructure to take you there. Move your strategy from the page to the product.

Design Your Solution Now

Contact Us

Schedule The Appointment At Your Convenience Date And Time.

30 Min

Web Conference

Time Zone

Indian standard time (08:30pm)

Thanks For Getting In Touch!

You’ve Taken The First Step Toward Transforming Your Digital Presence. Our Experts Will Reach Out Shortly To Take It Forward.

Launch Your Dream Project

Provide a brief overview of your project, and our specialists will evaluate your requirements. We will connect with you to explore how the right digital solutions can help you launch faster.